Eurozone: Measures to address the gas crisis and ongoing uncertainty are likely to stall GDP growth. US and UK: solid figures and record inflation are forcing central banks to put on the brakes. China’s real estate sector is worse than expected; infrastructure as a new growth driver.

Chart of the month

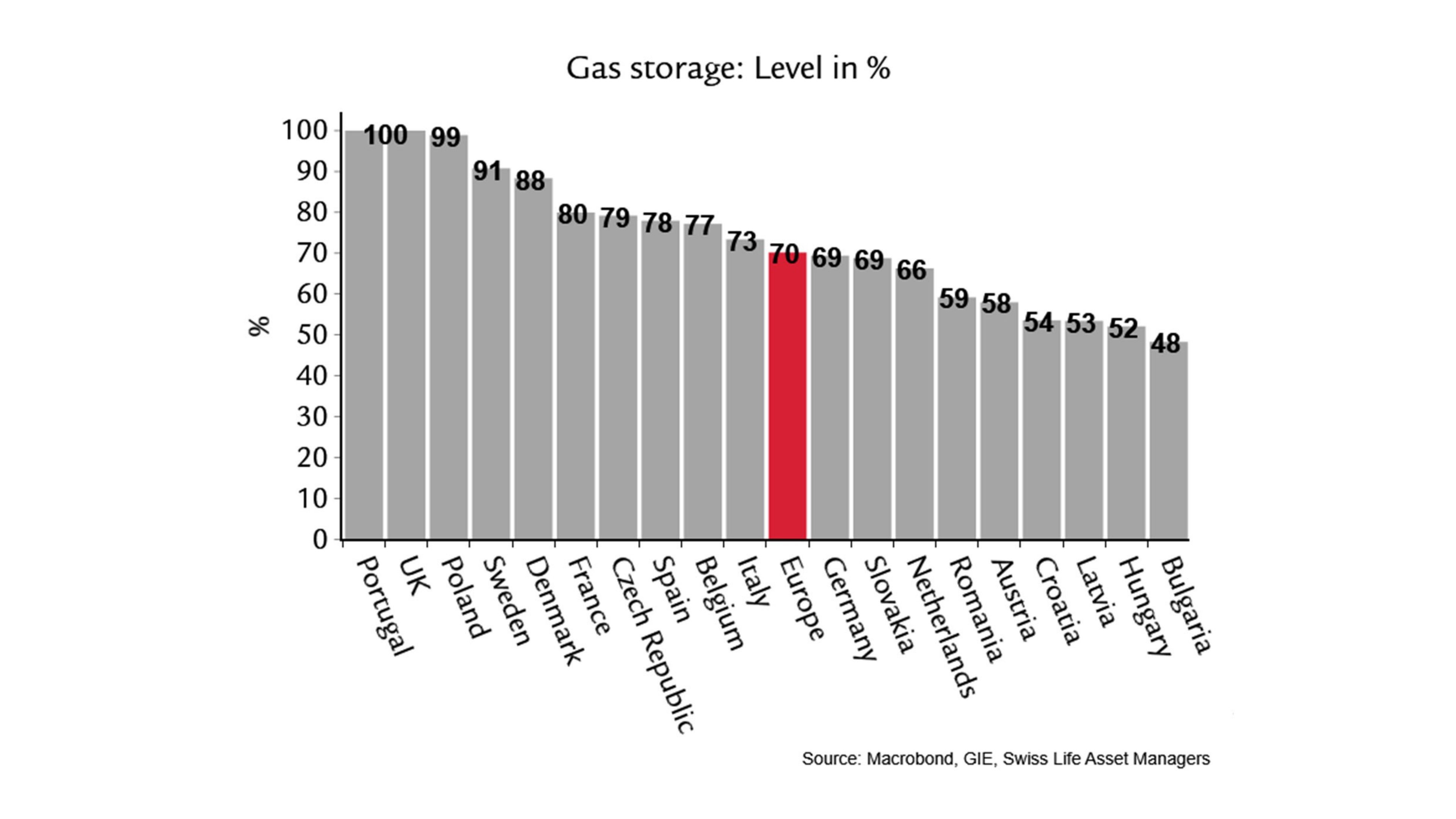

Everyone is currently talking about the filling levels of the gas storage tanks. But be careful with the interpretation: the UK has full gas storage facilities, but these are vanishingly small compared to consumption, while Austria’s half-empty gas storage facilities cover half of the country’s annual consumption. Throughout Europe, countries are on track to reach the 80% level required by the European Commission on 1 November. According to experts, this should be enough even in the event of a Russian gas supply stop this winter (with accompanying measures). In this worst-case scenario, however, the question of how to replenish the storage facilities for the winter of 2023/24 remains open – and has hardly been discussed so far.